Managing money each month can feel overwhelming, especially when bills, savings goals, and everyday spending compete for attention. Many households struggle not because they lack income, but because they lack structure. The 50/30/20 budgeting rule offers a clear and simple framework for organizing monthly finances. By dividing after-tax income into three main categories, the 50/30/20 method creates balance, encourages savings, and reduces confusion around spending decisions.

What Is the 50/30/20 Budgeting Rule?

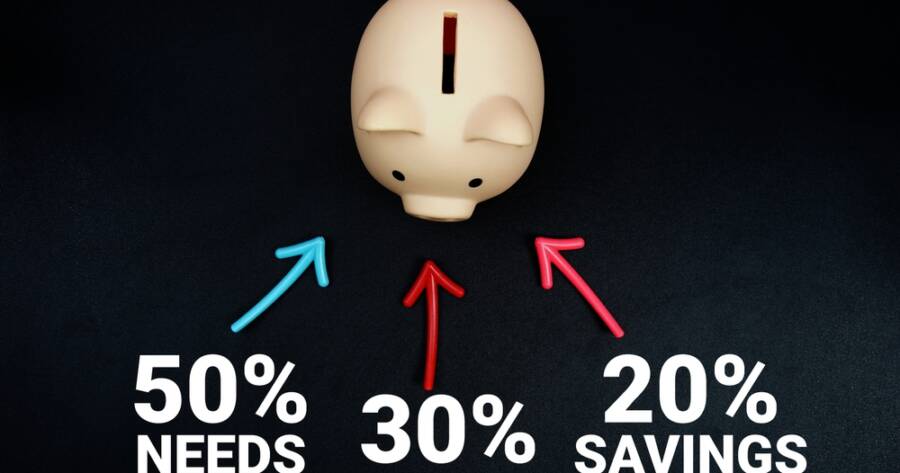

The 50/30/20 rule divides your after-tax income into three categories: 50 percent for needs, 30 percent for wants, and 20 percent for savings and debt repayment. This structure provides a broad guide rather than a strict formula, making it flexible for different income levels and lifestyles.

“Needs” include essential expenses that you must pay to maintain basic living standards. “Wants” cover non-essential spending that improves comfort or enjoyment. The final 20 percent focuses on financial progress through savings or paying down debt. By separating money into these clear groups, the rule simplifies decision-making and creates a steady financial plan.

Understanding the 50 Percent for Needs

The largest portion of your income, up to 50 percent, goes toward essential expenses. These typically include housing, utilities, groceries, insurance, transportation, and minimum debt payments. If you would struggle to live without the expense, it likely falls into the “needs” category.

Tracking these costs carefully is important because they form the foundation of your budget. If your needs exceed 50 percent of your income, you may need to review certain expenses. This could mean comparing housing options, adjusting grocery habits, or reviewing recurring bills. The goal is not perfection but awareness and gradual improvement.

Defining the 30 Percent for Wants

The 30 percent category covers discretionary spending. These are expenses that add enjoyment but are not required for survival. Dining out, entertainment, streaming services, vacations, hobbies, and shopping often fall into this group.

Separating wants from needs helps prevent guilt around spending. When you know that a set portion of income is designed for enjoyment, you can spend more confidently. At the same time, the limit protects long-term financial stability by preventing overspending in non-essential areas.

Allocating 20 Percent to Savings and Debt

The final 20 percent focuses on future security. This category includes building an emergency fund, contributing to retirement accounts, saving for major purchases, or paying more than the minimum on debts. It represents progress rather than maintenance.

If you carry high-interest debt, directing this portion toward repayment can reduce long-term financial pressure. Once debt is under control, shifting more of this percentage toward savings strengthens financial resilience. Over time, this steady habit builds stability and reduces stress around unexpected expenses.

How to Apply the Rule to Your Income

Begin by calculating your total monthly income after taxes. This number forms the base for your percentages. Multiply your after-tax income by 0.50, 0.30, and 0.20 to determine your spending targets for each category.

Next, review your recent bank and credit card statements to see how your current spending compares. Assign each expense to one of the three categories. This step may reveal imbalances, such as wants exceeding 30 percent or savings falling below 20 percent. Adjust gradually rather than making drastic changes all at once.

Using a spreadsheet or budgeting app can make tracking easier. Recording expenses weekly helps prevent surprises at the end of the month and keeps spending aligned with your targets.

Adjusting for Real-Life Situations

The 50/30/20 rule is a guideline, not a rigid command. In high-cost areas, essential expenses may temporarily exceed 50 percent. In that case, you may need to reduce discretionary spending until income grows or expenses decrease.

Life events such as job changes, new family members, or medical needs may also require adjustments. The strength of this method lies in its clarity. Even when percentages shift slightly, the three-category structure keeps finances organized and understandable.

Creating Clarity With a Simple Framework

Using the 50/30/20 budgeting rule to organize monthly finances brings structure to everyday money decisions. By dividing after-tax income into needs, wants, and savings, you create clear boundaries that guide spending and encourage long-term stability.

The system is simple enough to begin immediately yet flexible enough to adapt over time. With consistent tracking and small adjustments, this straightforward rule can help households build stronger financial habits and greater peace of mind. With the 50/30/20 method, you can allocate funds to your present needs and wants, as well as your future security.